The ERTC is a refundable credit that businesses can claim on qualified wages, including certain health insurance costs, paid to employees. The qualifying amount of the claim could be impacted by the laws that were in place at the time wages were paid, including:

healthCAR: Affordable Vehicle Protection for Your Vehicle’s Lifespan

Monday, June 05, 2023

Over the last few years, the cost of labor and automotive parts has continued to increase— leaving car owners with higher repair bills. With advanced electronics and computerized systems now standard in most vehicles, even the smallest repair can end up costing you hundreds, even thousands of dollars.

If you are looking to provide your children with a financial boost for their future, you might want to explore the benefits of opening an account that offers the flexibility to align the funds with their goals. A Uniform Transfers to Minors Act (UTMA) savings account might be precisely what you need.

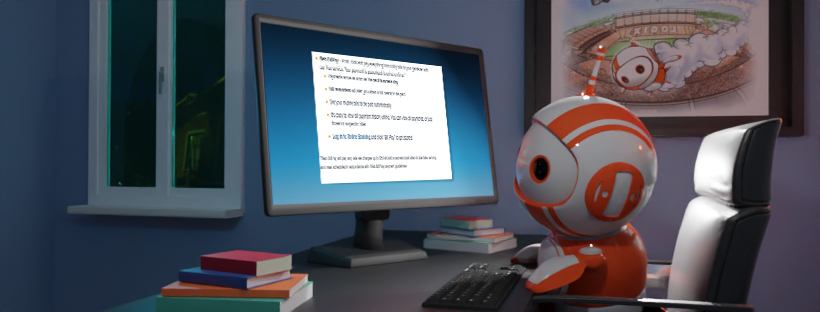

Yearning for a little bit of order in your life? When days are hectic and your brain is maxed out, having a tool that reminds you to pay your bills (or, pays your bills automatically) can be a huge relief.

Preventing Card Fraud: Freeze/Unfreeze Your Card in the Mobile App

Tuesday, May 23, 2023

Year after year, reports of debit and credit card fraud and associated financial losses continue to rise. As scammers become more skilled and sophisticated with their schemes, individuals need to enhance their digital security. So, how do you stay ahead of the game, you ask? Well, with the right knowledge and tools, of course. One powerful weapon is the ability to freeze or unfreeze your card using the Logix Mobile Banking app.

%20(1200%20x%20628%20px)%20(952%20x%20317%20px)-1.png)

%20(2)-1.png)

.png)

%20(952%20x%20317%20px)-2.png)